Investment Complexity and Operating Models

Boards of directors and investment committees of not-for-profit organizations serve many vital functions. One of their most important tasks is the implementation and monitoring of an organization’s investment program. This function is critical to protecting the organization’s assets and generating consistent returns that support its core mission in perpetuity.

Organizations are challenged in several key areas when it comes to their investment program:

In this article, we will discuss that final consideration: investment operating models. More specifically, we will look at the levels of complexity in various investable asset classes and investment operating models, highlighting what should be top of mind for organizations as they consider their investments.

Complexity by Asset Class

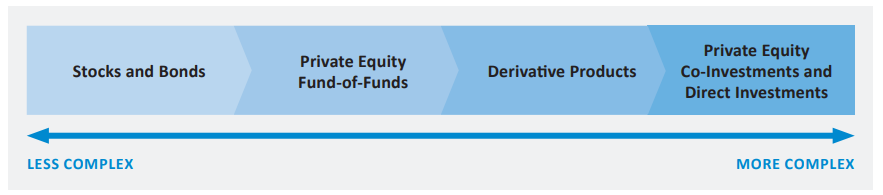

One of the biggest questions that organizations face is the extent to which they want to invest in complex asset classes.

Traditional publicly traded stocks and bonds tend to serve as the foundation for most investment portfolios. One reason is that these investments are generally straightforward—they can be purchased on regulated exchanges, are relatively liquid and can be held in various types of investment accounts. However, there are plenty of other investable asset classes that may help deliver the returns organizations desire.

This is just a snapshot of the options that are out there, though it does help illustrate the diversity of choice that organizations face.

All these assets classes have different risk/return characteristics, and generally speaking, as one moves from left to right on the diagram, they become less liquid and create a heavier middle- and back-office burden. These assets classes may all be compelling options, but it’s crucial that organizations consider their own risk/reward profile, long-term investment objectives and resource capacity.

Complexity in Operating Models—Commingled Funds vs. Separately Managed Accounts

Another area where organizations need to consider their capacity to manage complexity is the model by which they structure their investments. For many, this question boils down to the important choice between utilizing commingled funds or separately managed accounts (SMAs).

Investing in a commingled fund is a popular approach that many investors consider to be fairly simple. Through this structure, an organization invests in a fund where their assets are “commingled” with those of other investors. Common examples of commingled funds include mutual funds and exchange-traded funds (ETFs).

These funds can be accessed relatively easily by organizations, and logistics, like dividend management, are typically handled by the fund manager. This simplicity makes commingled funds a good option for investors of all shapes and sizes—even large institutional investors that want to avoid complex back-office tasks.

Alternatively, an organization may seek to structure its investments through an SMA. In an SMA, a third-party investment manager executes an investment strategy designed solely for that investor.

SMAs tend to be more customizable than commingled funds. For example, mission-focused organizations can enter into an SMA in which the investment manager excludes specific securities not aligned with that specific organization’s values. Another benefit of SMAs is that because the underlying investments are held at a custodian bank, an organization can decide to change their investment manager without selling their securities; they can transfer those securities to a new manager “in kind.”

However, SMAs also come with challenges and complexities. Most notably, organizations utilizing SMAs require the internal staffing resources to work with their custodian on reconciliations, corporate actions, dividends, tax reclaims, local market restrictions, securities lending and cash management. For this and other logistical reasons, SMAs are more often used by more sophisticated investors with the capacity to handle such tasks.